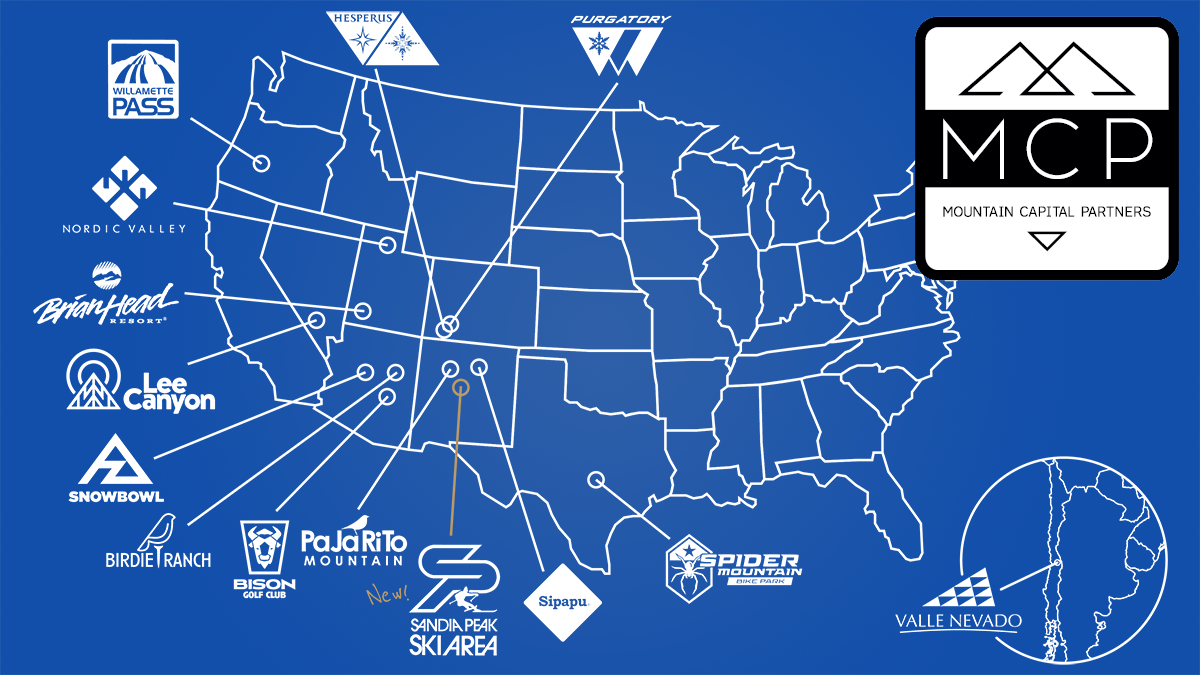

Mountain Capital Partners (MCP) is probably the biggest ski conglomerate that you have never heard of, at least in the East. With yesterday's announcement of their agreement to take over the operations of Sandia Peak Ski Area in New Mexico they now have 12 ski areas and several other recreational operations with a focus in the Southwestern United States. By some measures that makes them the third largest ski area operator in the US!

Sandia Peak Ski Area is located near Albuquerque, NM and did not operate for the last two seasons due to a what they described as a combination of weather and staffing challenges, and possibly was sacrificed in order to better staff the larger Ski Santa Fe. They rely primarily on natural snow with just 30 acres of snowmaking and at their far southern latitude they are at the whim of not just moisture flow, but also temperatures unlike most of the Rockies, and that environment is not going to improve (although they are due for a good year with a strong El Nino). The ski area needs more snowmaking to survive for the long-term, and water is scarce in this area. The long haul fixed grip doubles servicing the mountain also makes this area compare less favorably to Ski Santa Fe. The short operating seasons and limited summer operations are also the kiss of death for keeping experienced staff around who know how to make things hum because good staff require more than a unreliable seasonal job. Mountain Capital Partners is taking over just the ski operations leaving the tram, land, and facilities ownership in the hands of the Abruzzo family who will continue to operate the tram at Sandia as well as nearby more popular Ski Santa Fe. It seems likely that there will be plans to invest in both snowmaking and lifts at Sandia because that is what it will take to make this ski area more competitive, and that's what MCP specializes in on a smaller scale. The area may also be prime for some downhill mountain biking in the summer and MCP has experience in those operations as well.

Mountain Capital Partners is on a roll in closing deals recently. Just about a year ago they took over operations at Willamette Pass in Oregon and also announced an expansion to about double the size of the resort, and this April they became the majority owner of Valle Nevado in Chile, a leading southern hemisphere destination. This makes them the third largest ski conglomerate in the US behind Vail Resorts and Alterra by raw numbers of ski areas with 12 now owned and/or under management (11 in the US), but probably behind both Boyne (10 US ski resorts) and POWDR Corp. (9 US ski resorts) in overall skier visits. This also begs the question, what will happen to Ski Santa Fe which sells their own pass and is now in competition with Sandia Peak nearby? There could be another opportunity in the future and possibly deeper ownership should things work out at Sandia, though the US Forest Service's lease for the land requires it to operate for skiing and eventually they would have moved to cancel their lease. So having another operator come in to use their infrastructure and turn this place profitable is a better result than losing the lease to another owner over which you have no influence.

Mountain Capital Partners has apparently been poking around in the East, though we are not sure how seriously. They have yet to invest in any ski operations west of the Rockies but have begun to venture outside of the Southwest with their last two transactions into Oregon and Chile; suggesting their strategy has started to change.

Potential Target for Partnerships and Acquisitions

What really piques our interest is the opportunity that partnering with or buying out a company like this could do for either Alterra or Vail Resorts and their respective passes, and how that might affect the landscape. That's not to say that this is what Mountain Capital Partners desires or would accept, but Vail Resort's success with urban feeders and medium-sized mountains have made these places sexy again as acquisition targets and part of a broader strategy to funnel people to destination markets. What they are looking for the most are turnkey operations with healthy business and selling at a nice premium, while MCP is more of a turn-around type of operator.

A pairing with either's pass would have similar effects on the Southwest to Vail Resorts buying out Peak Resorts in the Northeast and Midwest several years ago; creating the East Coast's most popular pass out of nowhere and adding a significant boost to their business despite none of the resorts being true destinations and many of them quite small. When you add partners to a pass it may not add actual value to most, but it does create the perception of value which does help to sell more ski passes.

Vail Resorts would typically seek to purchase outright a company like this as they primarily provide unlimited access on their passes except in a few select markets where they desire to be more competitive and cannot or do not want to purchase the competition. Likely the value of MCP is at least a couple hundred million, but this would do for Vail Resorts pretty much what Peak Resorts did for them in laying claim to the East and it's an intriguing possibility that could make great business sense for them to explore. It bares mentioning that selling out to Vail Resorts can be unpopular among some, and this may be limiting their opportunities to grow domestically. It also bares mentioning that they would practically own three major metropolitan markets if they did while adding a destination in South America which they do not already have.

Alterra has probably a more compelling reason to partner with or purchase Mountain Capital Partners. With Windham, Mt. Bachelor, Alyeska, Blue Mountain, and Camelback joining Ikon Pass in the past three years as limited pass partners this signals a change in Alterra's strategy concerning pass partners and shows that they are willing to consider some leading resorts in drive-to regional markets as opposed to just destinations. Adding MCP to Alterra's portfolio would act as a gateway from urban centers like Las Vegas, Phoenix, and Albuquerque to their destinations just like Vail Resorts has done in other areas. It also doesn't hurt that MCP-controlled Valle Nevado is already a partner on the Ikon Pass. If Alterra wants to compete more broadly in the multi-pass wars, they need to acquire some more urban feeders, but they also need to rethink their pass structures and introduce things like a weekday pass, less expensive passes for smaller less popular mountains, and a more expensive pass that accommodates the needs of leading resorts like Jackson Hole and Aspen rather than this add-on stuff

There are other possibilities also including a merger with another operator like Boyne or POWDR to provide even more economies of scale and value to their products. It's hard to predict exactly how a marriage with MCP might happen in the end, but it would surely be seismic for the Southwest ski industry should one occur and it would reverberate through the entire ski industry as new lines are drawn.

Competitive As a Medium-Sized Mountain Conglomerate

Now Mountain Capital Partners likely did not build their portfolio with an intention of selling it to the highest bidder, but they also probably didn't expect the industry to look like what it does now when they started. They offer their own Powder Pass which provides access to all of their resorts and is a major contender in the NV, AZ, and NM local ski markets. They offer great value to families as well with a free pass product for kids 12 and under. They specialize in medium-sized resorts and ones that are closer to big cities. While they may not be destinations, ski areas located close to large cities tend to do extremely well when also operated well or otherwise have little competition.

Mountain Capital Partners can of course keep chugging along quietly if they wish, while leveraging their network and continuing to grow their multi-pass product that can accommodate both local and destination skiing with the addition of a few pass partners. Their goal may be simply to make money saving these places and not to make money by flipping them. We do see opportunity in the Northeast for a player at the mid-levels of the industry and while it seems unlikely to happen, with the right moves they could quickly establish themselves as another alternative. It would be a bold move to enter the East, but they have been pretty active and expanding their focus recently, and operating contracts are much less expensive upfront than buying resorts as a whole. One way or another, watch these folks because they are making moves!

Comments ()